As the transition toward zero-emission electrified mobility accelerates, monitoring the automotive market becomes a useful reference point for assessing manufacturers’ strategies in response to the new emission reduction targets.

In order to provide reliable and up-to-date data to the public debate, the think tanks Agora Verkehrswende (Germany), alinnea (Spain), ECCO Climate (Italy), the International Council on Clean Transportation (ICCT), the Mobility in Transition Institute (IDDRI-IMT, France), and the Polish Association for New Mobility (PSNM, Poland) publish monthly data on the average specific emissions of newly registered vehicle fleets in the European Economic Area, both overall and by country. These data make it possible to track manufacturers’ compliance gap with respect to the CO₂ reduction targets (Regulation 2019/631) set for the 2025–2027 period, as well as the reduction of CO₂ emissions from new vehicles through 2035.

alinnea provides the report data with a particular focus on Spain, the fourth-largest automotive market in Europe.

The monitoring includes details on registrations by powertrain type: battery electric vehicles (BEV), plug-in hybrid vehicles (PHEV), full hybrids (HEV), and mild hybrids (MHEV), as well as a quarterly update on: the evolution of charging infrastructure, the production, purchase, and registration of vans, and corporate electric vehicles.

Through these updates, our objective is to provide a useful tool for automobile manufacturers, analysts, public administrations, trade unions, and environmental organizations. In short, all stakeholders involved in the transition toward zero-emission mobility.

The European Car Market Monitor will be published each month on alinnea’s website and will be distributed to the media and to members of the alinnea Community involved in electric mobility.

Spanish market

CO₂ emissions from the sector

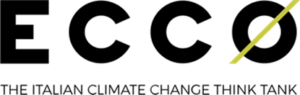

The average share of battery electric vehicles (BEVs) among total new registrations in Europe reached 19% in January–February 2026, matching the 2025 average and marking a 3-percentage-point increase compared with the same period in 2025 (see Figure 1).

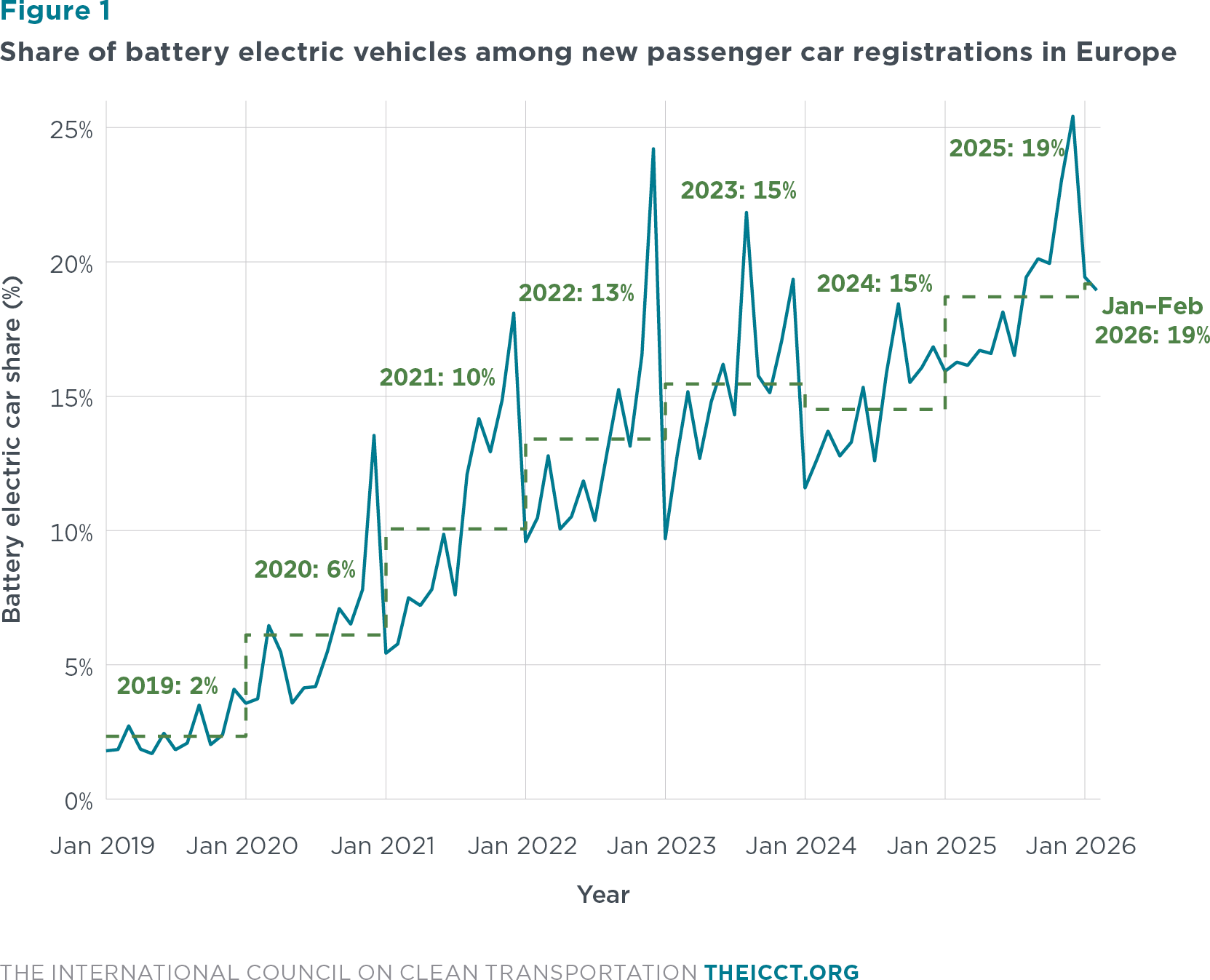

In January–February 2026, plug-in hybrid vehicles (PHEVs) had an average market share of 10% among new registrations in Europe, up 3 percentage points from January–February 2025.

Compared with the same period in 2025, full hybrid (HEVs) and mild hybrid electric vehicles (MHEVs) increased in market share by 1 and 3 percentage points, respectively, in January–February 2026, reaching shares of 14% and 26%. Meanwhile, conventional internal combustion engine vehicles (ICEVs) comprised 31% of new registrations in January–February 2026. This is 9 percentage points lower than in the same period in 2025 (see Figure 2).

Of the 10 largest European markets, Italy registered the biggest increase in total new car registrations (+14%) and the Netherlands the largest decrease (−19%) in February 2026, compared with February 2025 (see Table A5 in the Appendix).

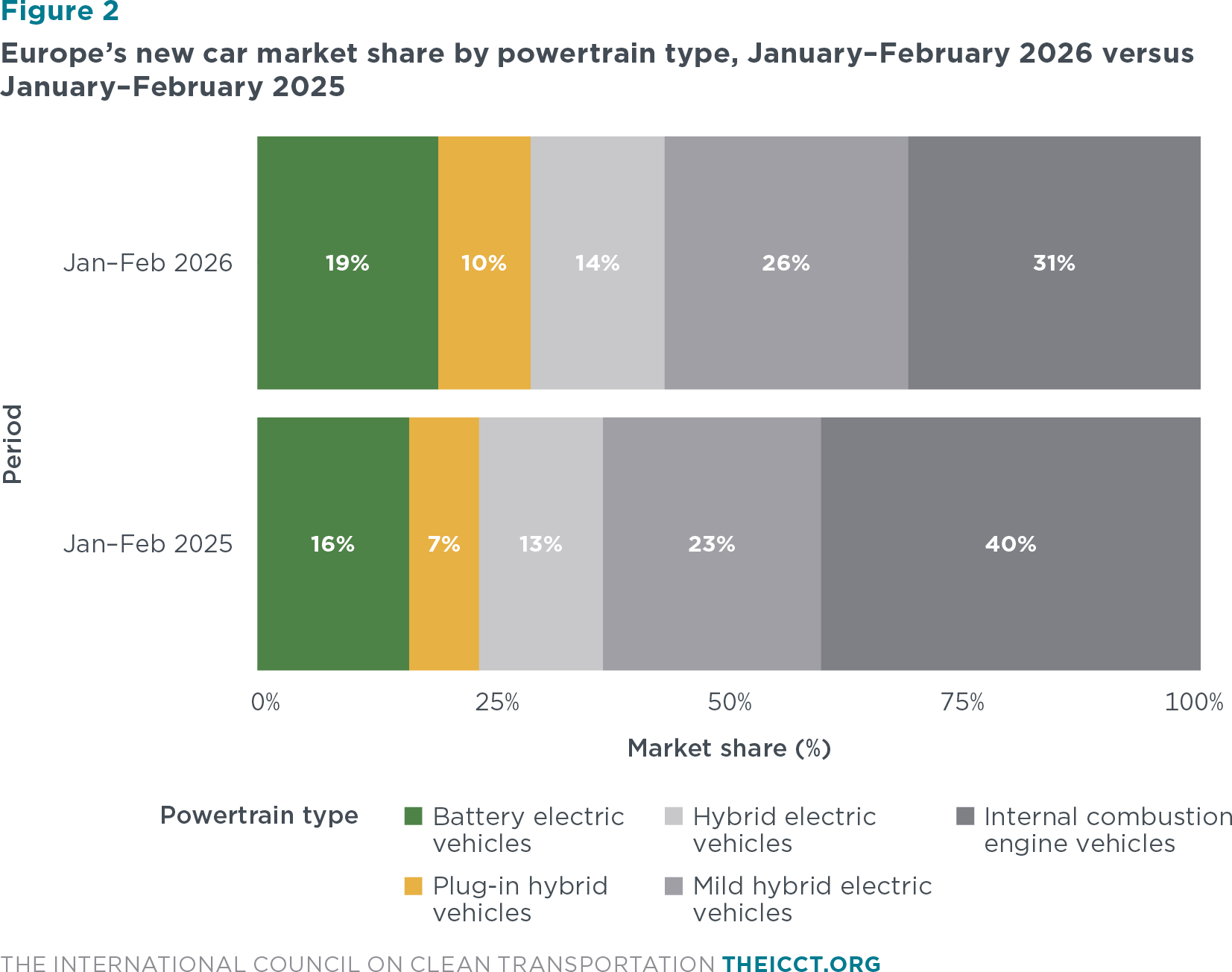

Looking at new BEV registrations in January–February 2026, Germany and France had BEV market shares of 22% and 27%, respectively. This represents increases of 5 and 9 percentage points compared with the same period in 2025.

Italy and Spain, the third and fourth largest markets, each had increases of 2 percentage points, reaching BEV shares of 7% and 9%, respectively, in January–February 2026.

Nordic countries and Belgium led Europe’s battery electric car registration shares in January–February 2026 (Figure 3). While Norway and Denmark already surpassed the 50% mark at 97% and 82%, respectively, Finland (45%), Sweden (40%), Belgium (33%), the Netherlands (27%), France (27%), Luxembourg (26%), and Portugal (25%) all had BEV shares of 25% or greater. Also with BEV market shares above of the European average were Iceland (23%), Germany (22%), and Austria (21%). In January–February 2026, Denmark had the greatest increase in market share compared with the same period in the previous year (+17 percentage points).

Looking at other drivetrains in the 10 largest European markets, PHEV shares were the highest in the Netherlands (27%) and Spain (12%) in January–February 2026. Poland (25%) and France (23%) had the highest HEV shares, while MHEV shares were the highest in Italy, at 37%, followed by Poland with 27%.

Under EU regulation, Europe’s carmakers are required to reduce their CO2 emissions from new cars incrementally until 2035. The current target value applies for each year from 2025 to 2029. However, compliance with the targets will first be assessed at the end of 2027 and will consider average new car fleet CO2 emissions from the 2025–2027 period. Automakers are permitted to combine their emissions performance across these 3 years through pooling arrangements (manufacturing pools) and may use compliance credits earned by selling zero- and low-emission vehicles (ZLEVs) as well as by deploying eco-innovations (i.e., technologies that deliver real-world CO2 savings beyond what is measured over the standardized test cycle during type approval). Increasing the share of battery electric cars is the leading strategy used by manufacturers to achieve these reductions and avoid penalties.

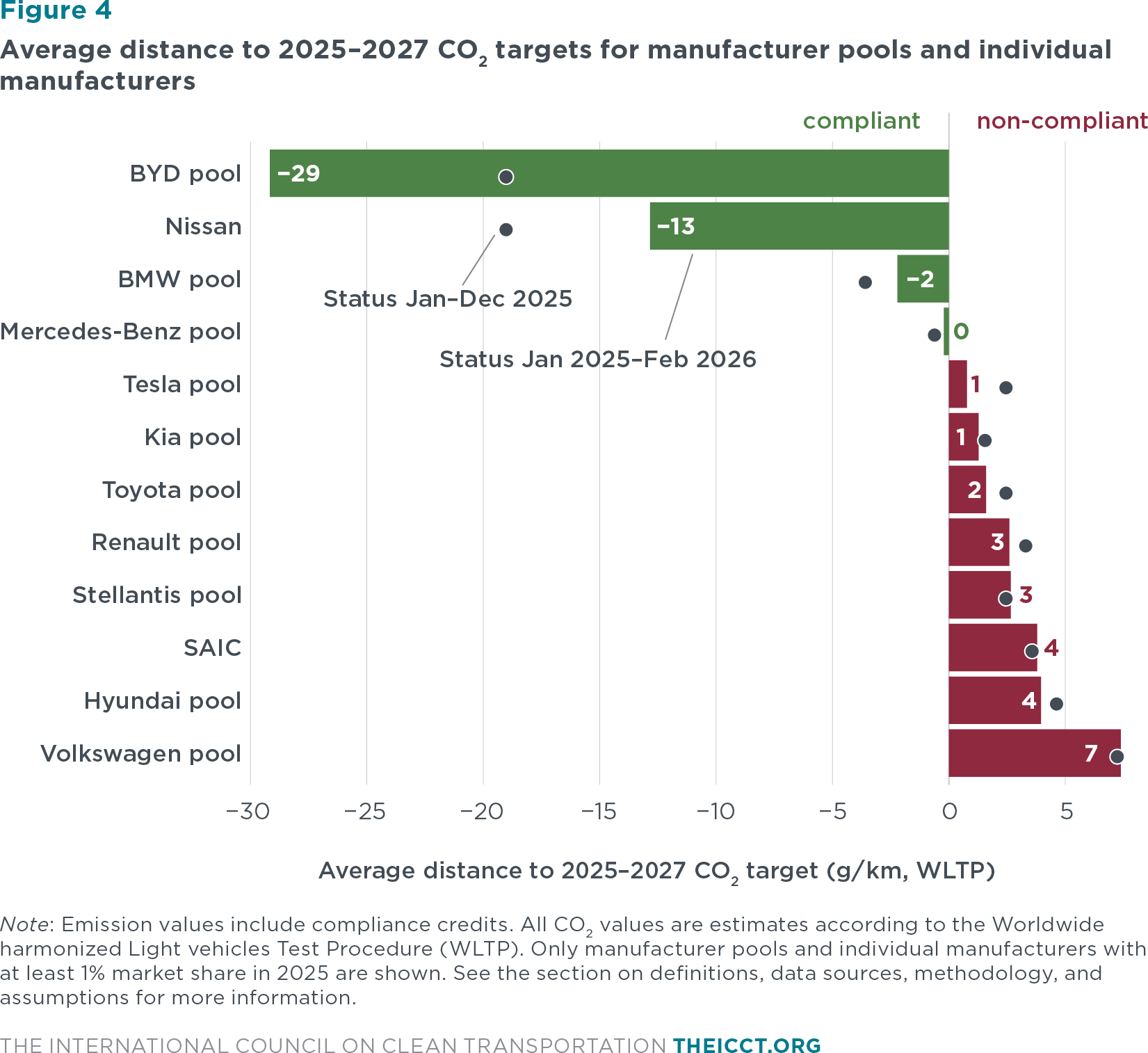

In January–February 2026, manufacturer CO2 emissions averaged 97 g CO2/km. After accounting for compliance credits, manufacturers were, on average, 3 g CO2/km above the 2026 target (see Table A2 of the Appendix). For the reporting period from January 2025 to February 2026, adjusted emissions stood at 97 g CO2/km. Including compliance credits, manufacturing pools thus remained 4 g CO2/km short of the average target of 93 g CO2/km for the 2025–2027 period, unchanged from the target gap recorded in 2025 (see Table A3 in the Appendix).

For the January 2025–February 2026 period, the BYD pool (29 g CO2/km below), Nissan (13 g CO2/km below), the BMW pool (2 g CO2/km below), and the newly formed Mercedes-Benz pool (at target), which includes Volvo, were all meeting their 2025–2027 targets, while the Volkswagen pool (+7 g CO2/km) remained the farthest from its target (see Figure 4).

The BYD and Tesla pools had the largest BEV registration shares in February 2026, at 45% and 33%, respectively. The Mercedes-Benz (27%), Kia (23%), BMW (23%), and Hyundai (21%) pools also had shares above the European average. Nissan (7%), the Toyota pool (8%), and SAIC (11%) had the lowest BEV shares in February (see Table A1 in the Appendix).

Looking at individual car brands with market shares of 1% or greater, Tesla and BYD had the greatest over-compliance at 92 g CO2/km and 81 g CO2/km, respectively, below their projected brand-level average targets for 2025–2027, followed by Volvo (30 g CO2/km below), Mini (19 g CO2/km below), and Cupra (17 g CO2/km below). The brands with the largest target gaps were Nissan (28 g CO2/km above), SEAT (24 g CO2/km above), Mercedes-Benz (20 g CO2/km above), and Mazda (19 g CO2/km above; see Table A4 of the Appendix).

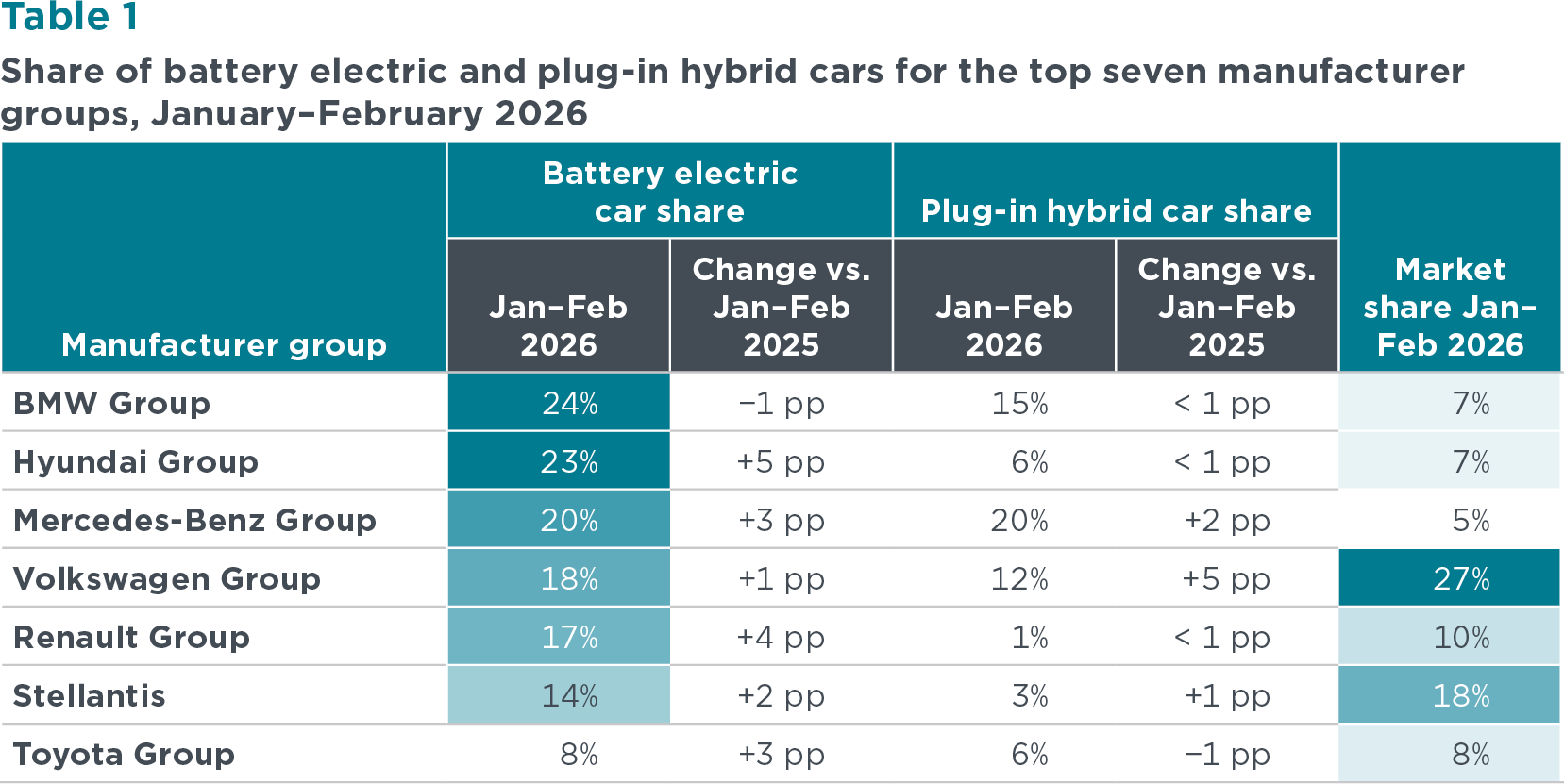

Among the largest carmakers, the Hyundai Group had the greatest increase in BEV market share in January–February 2026, increasing 5 percentage points compared with January–February 2025 (Table 1). With a 27% market share in January-February 2026, the Volkswagen Group increased its PHEV share by 5 percentage points over the same period in 2025.

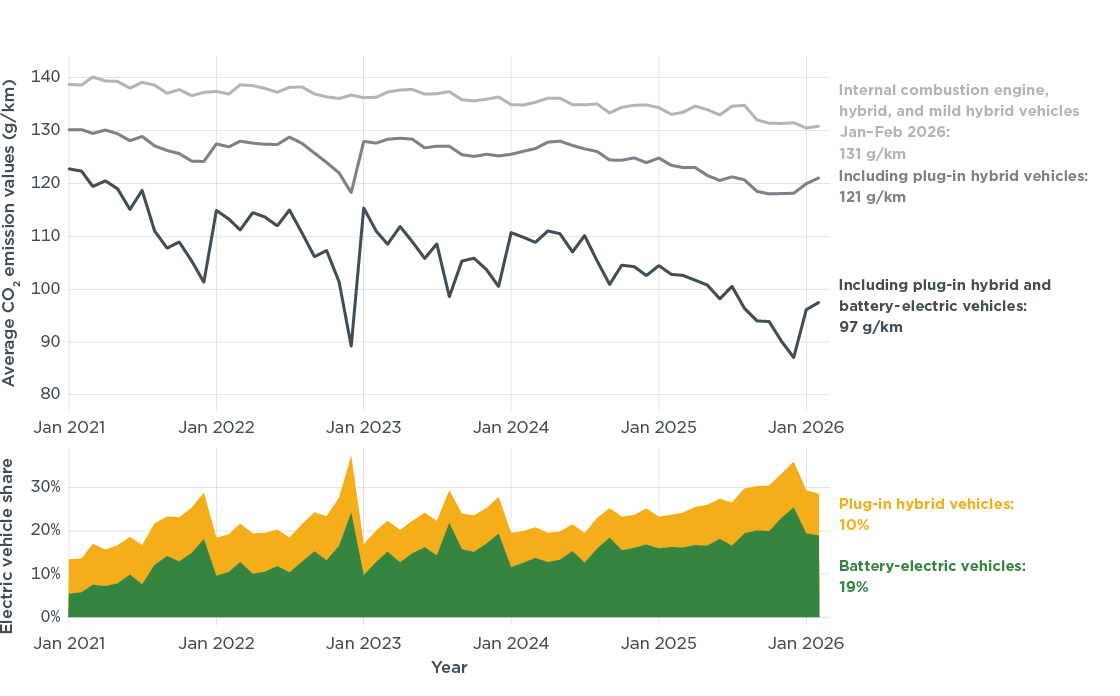

Of all powertrain types, battery electric cars have the largest potential to reduce total CO2 emissions.2 When looking at new registrations of ICEVs (including HEVs and MHEVs) alone, CO2 emissions averaged 131 g CO2/km in January–February 2026. Including PHEVs reduced the average to 121 g CO2/km, while the increasing market share of BEVs reduced average CO2 emissions by an additional 24 g CO2/km in January–February (see Figure 5).

Figure 5

Average CO₂ emissions of newly registered internal combustion engine vehicles

and reductions in the fleet average associated with the uptake of electrified powertrains

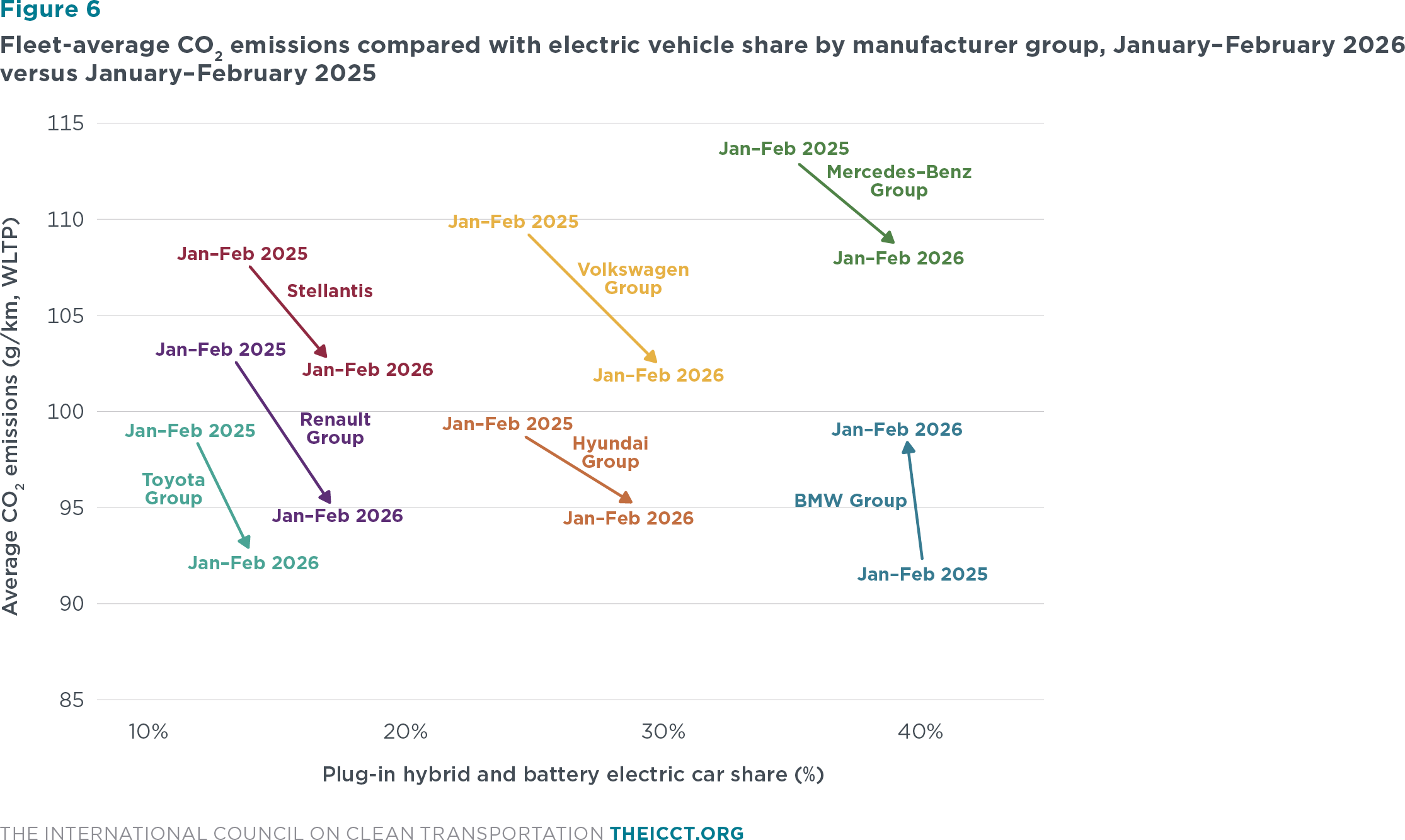

Looking at the relationship between electric car shares and average CO2 emissions, the Mercedes-Benz group had the highest average emissions of the top manufacturers in Europe while having the second highest share of PHEVs and BEVs in January–February of 2025 and 2026. This is largely dueto the high average CO2 emissions of the group’s non-electrified powertrains, which stood at about 165 g CO2/km in January–February 2026, the highest level among Europe’s largest carmaker groups. Although the BMW Group had consistently low fleet emissions in 2025, it has seen higher emissions in 2026 due to slightly lower BEV shares and an increase in recorded PHEV emissions to more realistic levels resulting from the European Commission correction of the electric driving share assumed for type-approval. With its focus on hybrid powertrains, Toyota had average CO2 emissions meeting the 2026 target in January–February despite maintaining the lowest electric vehicle share (see Figure 6)

The think tanks Agora Verkehrswende (Germany), alinnea (Spain), ECCO Climate (Italy), the International Council on Clean Transportation (ICCT), the Mobility in Transition Institute (IDDRI-IMT, France), and the Polish Association for New Mobility (PSNM, Poland) publish monthly data on the average specific emissions of newly registered vehicle fleets in the European Economic Area, both overall and by country.

These data make it possible to track manufacturers’ compliance gap with respect to the CO₂ reduction targets (Regulation 2019/631) set for the 2025–2027 period, as well as the reduction of CO₂ emissions from new vehicles through 2035.

alinnea provides the report data with a particular focus on Spain, the fourth-largest automotive market in Europe.