As the transition to zero-emission electrified mobility accelerates, monitoring developments in the automotive market becomes an important benchmark for assessing how manufacturers are adapting their strategies to meet increasingly stringent emissions reduction targets.

To provide reliable and up-to-date data to the public debate, the think tanks Agora Verkehrswende (Germany), alinnea (Spain), ECCO Climate (Italy), the International Council on Clean Transportation (ICCT), the Institute for Mobility in Transition (IDDRI-IMT, France), and the Polish New Mobility Association (PSNM) publish monthly data on the average specific emissions of newly registered vehicle fleets across the European Economic Area, both at the aggregate and country level.

These data make it possible to track manufacturers’ compliance gap with the CO₂ reduction targets set for the 2025-2027 period under Regulation (EU) 2019/631, as well as progress towards the reduction of CO₂ emissions from new vehicles through to 2035.

alinnea provides the report’s findings with a particular focus on Spain, Europe’s fourth-largest automotive market.

The monitoring also includes detailed registration data by powertrain type, covering battery electric vehicles (BEVs), plug-in hybrid electric vehicles (PHEVs), full hybrids (HEVs), and mild hybrids (MHEVs). In addition, it provides a quarterly update on developments in charging infrastructure, the production, purchase and registration of vans, and the uptake of corporate electric vehicles.

Through these regular updates, our aim is to provide a valuable resource for automotive manufacturers, analysts, public authorities, trade unions, and environmental organisations. In short, for all stakeholders involved in the transition to zero-emission mobility.

The European Car Market Monitor will be published each month on alinnea’s website and will be distributed to the media and to members of the alinnea Community involved in electric mobility.

The Spanish Market

CO₂ Emissions from the Sector

¹ Geographic scope: To the extent permitted by data availability, the definition of Europe used in ICCT’s Market Monitor reports is aligned with EU regulations. European CO₂ standards for passenger cars and vans apply to the countries of the European Economic Area (EEA), with the exception of Liechtenstein. This includes the 27 Member States of the European Union, as well as Iceland and Norway.

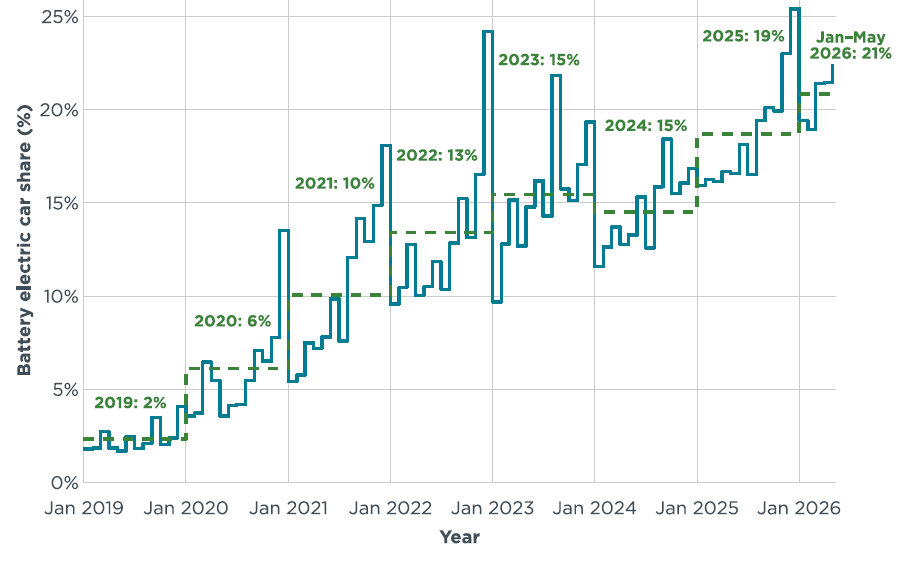

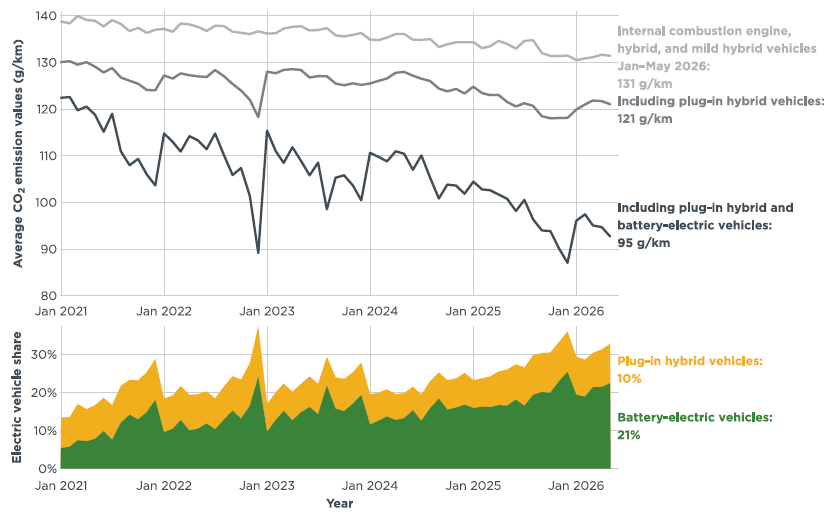

In May 2026, new battery electric car registrations reached a 22% market share out of all new registrations. This brought the average share of BEVs among total new registrations in Europe to 21% in January–May 2026, surpassing the 2025 average and marking a 5-percentage-point increase compared with the same period in 2025 (see Figure 1).

Figure 1

Share of battery electric vehicles in total new passenger car registrations in Europe.

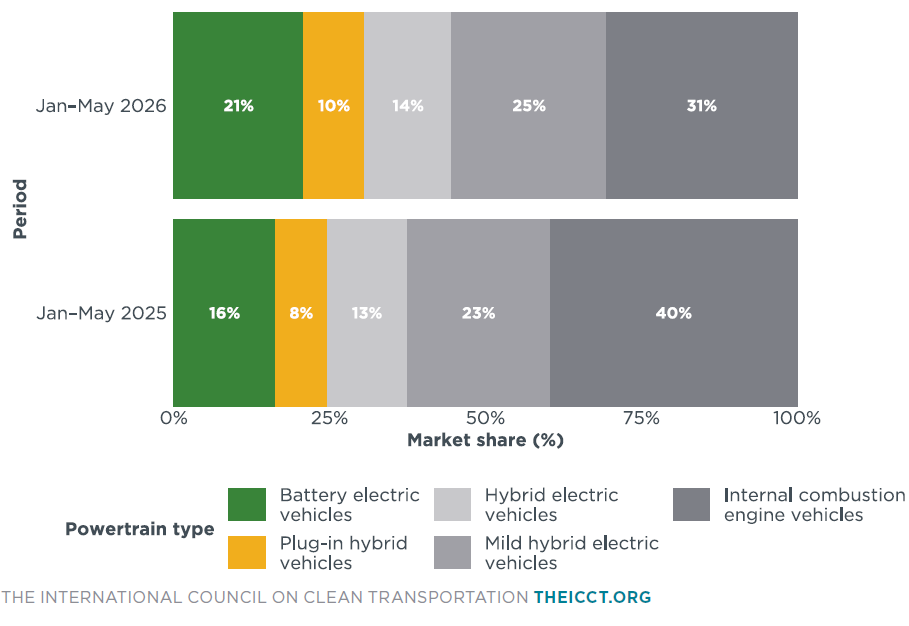

In January–May 2026, plug-in hybrid vehicles (PHEVs) had an average market share of 10% among new registrations in Europe, up 2 percentage points from January–May 2025.

Compared with the same period in 2025, full hybrid electric vehicles (HEVs) and mild hybrid electric vehicles (MHEVs) increased in market share by 1 and 2 percentage points, respectively, reaching shares of 14% and 25% in January–May 2026. Meanwhile, conventional internal combustion engine vehicles (ICEVs) comprised 31% of new registrations in January–May 2026. This is 9 percentage points lower than in the same period in 2025 (see Figure 2).

Figure 2

Market share of new passenger cars in Europe by powertrain type, January-April 2026 compared with January-May2025.

Total new registrations increased in many of the 10 largest European markets in January–May 2026, with Austria and Denmark recording the biggest increase among the largest markets compared with January–May 2025 (see Table A5 in the Appendix).

Looking at new BEV registrations in January–May 2026, Germany and Italy—currently Europe’s largest car markets—had BEV market shares of 24% and 8%, respectively. These represent increases of 6 and 3 percentage points, respectively, compared with the same period in 2025.

France and Spain, the third- and fourth-largest markets, had increases of 10 and 2 percentage points in January–May 2026, reaching BEV shares of 28% and 9%, respectively.

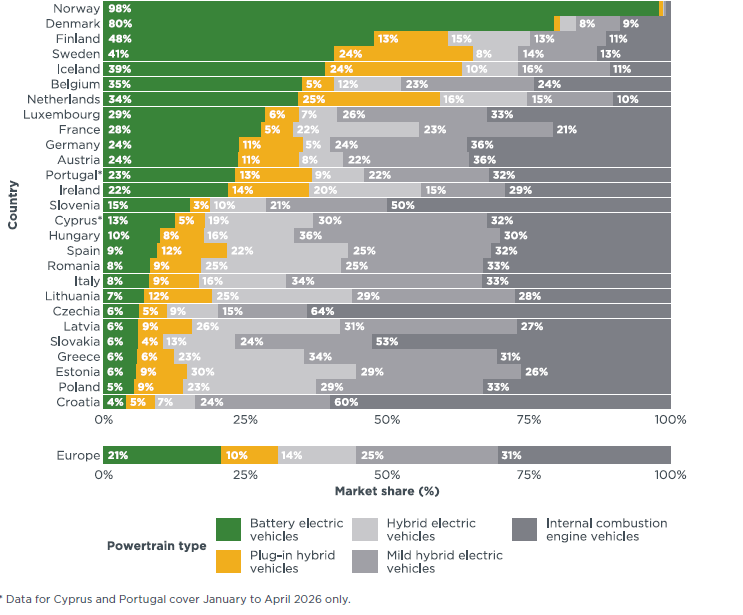

Nordic countries led Europe’s battery electric car registration shares in January–May 2026, with Norway and Denmark already reaching shares of 98% and 80%, respectively, followed by Finland (48%) and Sweden (41%; Figure 3). Iceland (39%), Belgium (35%), the Netherlands (34%), Luxembourg (29%), and France (28%) all had BEV shares of 25% or greater. In January–May 2026, Denmark recorded the greatest increase in BEV market share compared with the same period in the previous year (+17 percentage points).

Figure 3

Europe’s new car market share by country and powertrain type, January–May 2026

Looking at other powertrains in the 10 largest European markets, PHEV shares were the highest in the Netherlands (25%) and Sweden (24%) in January–May 2026. Poland (23%), France and Spain (both 22%) had the highest HEV shares, while MHEV shares were the highest in Italy, at 34%, followed by Poland with 29%.

Under EU regulation, carmakers are required to reduce their CO2 emissions from new cars incrementally through 2035. The current target value applies for each year from 2025 to 2029. However, compliance with the targets will first be assessed at the end of 2027 and will consider average CO2 emissions for new car fleets over the 2025–2027 period. Automakers are permitted to combine their emissions performance across these 3 years through pooling arrangements (manufacturing pools) and may use compliance credits earned by selling zero- and low-emission vehicles (ZLEVs) as well as by deploying eco-innovations (i.e., technologies that deliver real-world CO2 savings beyond what is measured over the standardized test cycle during type approval). Increasing the share of battery electric cars is the leading strategy used by manufacturers to achieve these reductions and avoid penalties.

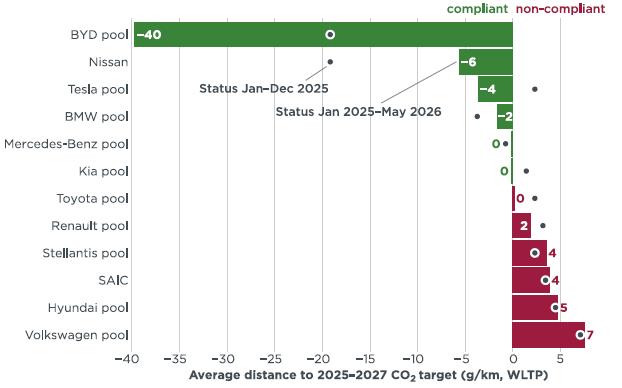

In January–May 2026, manufacturer CO2 emissions averaged 95 g CO2/km. After accounting for compliance credits, manufacturers were on average 2 g CO2/km above the 2026 target (see Table A2 of the Appendix). For the full reporting period from January 2025 to May 2026, adjusted emissions stood at around 96 g CO2/km. Including compliance credits, manufacturing pools thus remained 3 g CO2/km short of the average target of 93 g CO2/km for the 2025–2027 period, unchanged from the target gap recorded in 2025 (see Table A3 in the Appendix).

For the full January 2025–May 2026 reporting period, the BYD pool (40 g CO2/km below), Nissan (6 g CO2/km below), the Tesla pool (4 g CO2/km below) and the BMW pool (2 g CO2/km below), as well as the Mercedes-Benz, Kia and Toyota pools (at target) were all on track to meet their 2025–2027 targets, while the Volkswagen pool (+7 g CO2/km) remained the farthest from its targe

Figure 4

Average distance to 2025–2027 CO2 targets for manufacturer pools and individual manufacturers

Note: Emission values include compliance credits. All CO2 values are estimates according to the Worldwide harmonized Light vehicles Test Procedure (WLTP). Only manufacturer pools and individual manufacturers with at least 1% market share in 2025 are shown. See the section on definitions, data sources, methodology, and assumptions for more information.

The Tesla and BYD pools had the largest BEV registration shares in May 2026, at 41% and 35%, respectively. The Kia (32%), Mercedes-Benz (32%) and BMW (29%) pools also had shares above the European average of 22%. The Toyota pool (12%), SAIC (13%), and Stellantis pool (14%) had the lowest BEV shares in May (see Table A1 in the Appendix).

Looking at individual car brands with market shares of 1% or greater, Tesla and BYD had the greatest over-compliance at 92 g CO2/km and 76 g CO2/km, respectively, below their projected brand-level average targets for 2025–2027 at the end of May 2026, followed by Volvo (29 g CO2/km below), Mini (17 g CO2/km below), and Cupra (16 g CO2/km below). Nissan (27 g CO2/km above), SEAT (24 g CO2/km above), Mazda (20 g CO2/km above), Mercedes-Benz (19 g CO2/km above) and Fiat (18 g CO2/km above) had the largest target gaps (see Table A4 in the Appendix).

Among the largest carmakers, the BMW Group had the greatest BEV share in January–May 2026 at 27%. The Mercedes-Benz group increased its BEV share by 7 percentage points compared with January–May 2025, and the Hyundai, Renault, and Toyota groups all recorded increases in BEV shares of 5 percentage points, with Toyota doubling its share from 5% to 10% (Table 1). With a 26% market share in January–May 2026, the Volkswagen Group increased its PHEV share by 3 percentage points relative to the same period in 2025.

Table 1

Share of battery electric and plug-in hybrid cars for the top seven manufacturer groups, January–May 2026

| Manufacturer group | Battery electric car share | Plug-in hybrid car share | Market share Jan–May 2026 | ||

| Jan–May 2026 | Change vs. Jan–May 2025 | Jan–May 2026 | Change vs. Jan–May 2025 | ||

| BMW Group | 27% | +3 pp | 13% | -1 pp | 7% |

| Hyundai Group | 24% | +5 pp | 5% | -1 pp | 7% |

| Mercedes-Benz Group | 23% | +7 pp | 17% | -2 pp | 5% |

| Volkswagen Group | 19% | +1 pp | 12% | +3 pp | 26% |

| Renault Group | 17% | +5 pp | 1% | 0 pp | 10% |

| Stellantis | 14% | +2 pp | 2% | 0 pp | 17% |

| Toyota Group | 10% | +5 pp | 6% | -2 pp | 7% |

Of all powertrain types, battery electric cars have the largest potential to reduce total CO2 .[2] When looking at new registrations of ICEVs (including HEVs and MHEVs) alone, CO2 emissions averaged 131 g CO2/km in January–May 2026. Including PHEVs reduced the average to 121 g CO2/km, while the increasing market share of BEVs reduced average CO2 emissions by an additional 26 g CO2/km in January–May (see Figure 5).

Figure 5

Average CO2 emissions of newly registered internal combustion engine vehicles and fleet-average reductions associated with including electrified powertrains

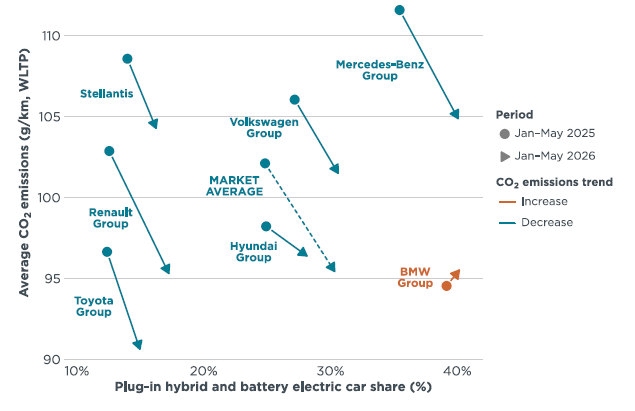

Looking at the relationship between electric car shares and average CO2 emissions, the Mercedes-Benz group had the highest average emissions of the top manufacturers in Europe while also having the highest combined share of PHEVs and BEVs in January–May 2026. This was largely due to the high average CO2 emissions of the group’s non-electrified powertrains, which stood at about CO2/km in January–May 2026, the highest level among Europe’s largest carmaker groups. As a counterexample, with its focus on hybrid powertrains, Toyota had average CO2 emissions below its 2026 target in January–May despite maintaining the lowest electric vehicle share.

Among Europe’s top manufacturers, the BMW Group is the only case where emissions increased in 2026 compared with the previous year. This disparity is due in part to an increase in recorded PHEV emissions to more realistic levels resulting from the European Commission correction of the electric driving share assumed for type approval at the beginning of the year. However, it also mirrors a trend observed in previous CO2 target cycles: without interim annual targets, manufacturers often scale back their CO2 reduction efforts once meeting their defined emissions target instead of using the momentum to reach the next target on a continuous reduction pathway. These delayed efforts have historically resulted in manufacturers claiming that the defined targets cannot be met and calling for last-minute policy action to weaken the targets (see Figure 6).[3]

Figure 6

Fleet-average CO2 emissions compared with electric vehicle share by manufacturer group, January–May 2026 versus January–May 2025

In Europe, corporate registrations account for about 60% of the new car market. This category includes all vehicles registered by legal entities rather than private individuals, such as company fleets of any size, rental fleets, and dealers’ and manufacturers’ self-registrations. Compared to privately owned cars, corporate vehicles tend to cover greater annual distances, resulting in higher total CO2 emissions. Further, they are typically turned over more quickly, subsequently entering the second-hand market and expanding access to electric vehicles for a wider range of consumers.[4]

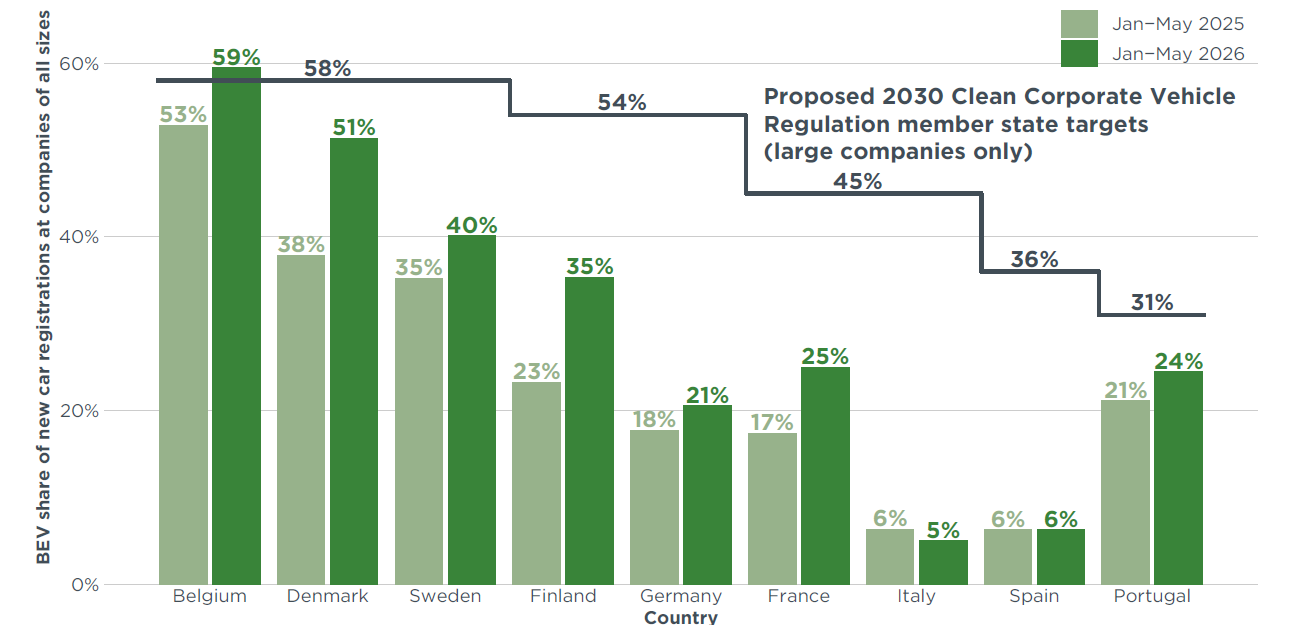

In Europe’s four largest car markets by new registrations (Germany, Italy, France and Spain), corporate BEV adoption has been no faster than, and in some cases slower than, that of private households.[5] To accelerate corporate uptake of zero- and low emission vehicles the European Commission put forward the proposal in December 2025.[6] The proposal sets binding fleet electrification targets for large companies[7] – however at the Member State and not at individual company level – for 2030 and 2035, with the aim of creating a predictable ZLEV demand, accelerating emissions reductions, increasing the availability of used ZLEVs.

Figure 7 shows the battery electric share of total corporate car registrations (across all company sizes) in January–May 2026 and January–May 2025 for 9 selected countries (J, compared with the CCVR proposed zero-emission car targets for large companies (250 employees and more) for 2030. While the targets apply specifically to large companies, ZLEV shares of the full corporate market Year-on-year, all countries except Italy and Spain saw an increase in their corporate BEV shares. Belgium stands out with a BEV share of 59% in total new corporate registrations in January–March 2026, slightly above the 2030 target level set for for large companies. Denmark, which shares the same target of 58%, reached a corporate BEV share of 51% in January–May 2026, slightly below the target benchmark. At the other end of the spectrum, Italy recorded a corporate BEV share of 5% in January–May 2026, which is substantially below the level envisaged for large companies by 2030.

Figure 7

Battery electric share in new corporate car registrations (all company sizes) for 9 selected European countries, January–May 2026 versus January–May 2025

Note: Data for Belgium cover January to March only. Proposed targets as part of the Clean Corporate Vehicles Regulation at Member State level (scope: large companies).

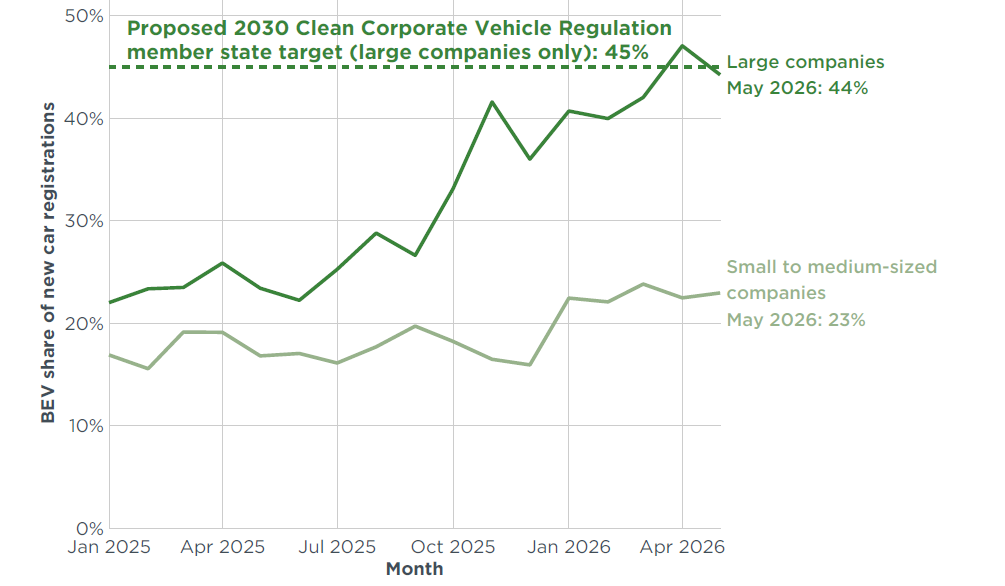

Figure 8 illustrates the evolution of BEV shares in large and small to medium-sized enterprises in France, allowing for a differentiated analysis of corporate BEV uptake and a direct comparison with the national 2030 CCVR proposal target. SMEs are defined as those with fewer than 250 employees. Between January 2025 and May 2026, large companies, which represent about 27% of total corporate registrations in France over that period, saw a steady increase in their BEV share, reaching 44% in May 2026. Notably, April marked the first month in which the 2030 target was surpassed, with a BEV share of 47%. For comparison, SMEs, which are showed a slower rate of adoption, reaching a BEV share of 23% in May . In light of the pronounced BEV advantage recorded by large companies in France, most countries are likely to be closer to their proposed CCVR targets than Figure 7 suggests.

Figure 8

Battery electric share in new corporate car registrations by company size January 2025–May 2026.

Note: Proposed targets under the Clean Corporate Vehicles Regulation are calculated at the Member State level (for large companies only). For source information, see the section on definitions, data sources, methodology, and assumptions.

The think tanks Agora Verkehrswende (Germany), alinnea (Spain), ECCO Climate (Italy), the International Council on Clean Transportation (ICCT), the Mobility in Transition Institute (IDDRI-IMT, France), and the Polish Association for New Mobility (PSNM, Poland) publish monthly data on the average specific emissions of newly registered vehicle fleets in the European Economic Area, both overall and by country.

These data make it possible to track manufacturers’ compliance gap with respect to the CO₂ reduction targets (Regulation 2019/631) set for the 2025–2027 period, as well as the reduction of CO₂ emissions from new vehicles through 2035.

alinnea provides the report data with a particular focus on Spain, the fourth-largest automotive market in Europe.